Global Export 2024/2025: first-half data

As the year draws to a close, it seems useful to take a look at the figures recorded in the first half of 2025 by the leading producing countries in terms of global exports.

No one can deny that this is, to say the least, a “confusing” season. Uncertainty has often taken on dramatic overtones and continues to affect economic trends at every level, regardless of the type of goods or services involved.

Woodworking technologies and the furniture industry are certainly no exception. The data processed by the Studies Office of Acimall, the association representing Italian companies in the sector, provide clear confirmation.

We have therefore decided to offer our readers a summary of the contents of this important report, which provides an extremely meaningful overview of the current trends.

Let us begin with a couple of general considerations relating to the period 2017–2024. First of all, the overall volume of global exports has not undergone major changes in recent years: it rose from €8.9 billion in 2017 to €10.8 billion in 2024, with two peaks in 2021 (€10.9 billion) and 2023 (€11.4 billion).

Some changes, even significant ones, can be observed when looking at the role of individual producing countries over the same period (Table 1): China is the leading exporter, a position it achieved in 2021 by overtaking Germany, which remains steadily in second place. The values recorded by the industry in the two countries are fairly close. In fact, in 2023 Germany briefly regained first position. However, this “head-to-head” seems to indicate a clear trend highlighting China’s growth also in the production of technologies for the wood supply chain — a global leadership that appears destined to consolidate further, especially in light of the current situation of the German economy.

Italy is also facing increasingly strong competition from Chinese supply and already lost second place in 2019. In the following years, it has firmly held third position in the exporters’ ranking, closing out a leading trio that has always maintained a considerable gap over the followers.

This gap between the top three and the rest of the ranking clearly emerges from Table 1, which also shows China’s advance — interrupted only in 2023, when exports fell from €2.82 billion in 2022 to €2.30 billion — compared with the substantial stability of Germany and Italy. As mentioned, the gap from the next countries — primarily Austria and Taiwan — remains significant, as they account for about one-third of Italy’s exports and one-fifth compared with the leading country.

THE FIRST HALF OF 2025

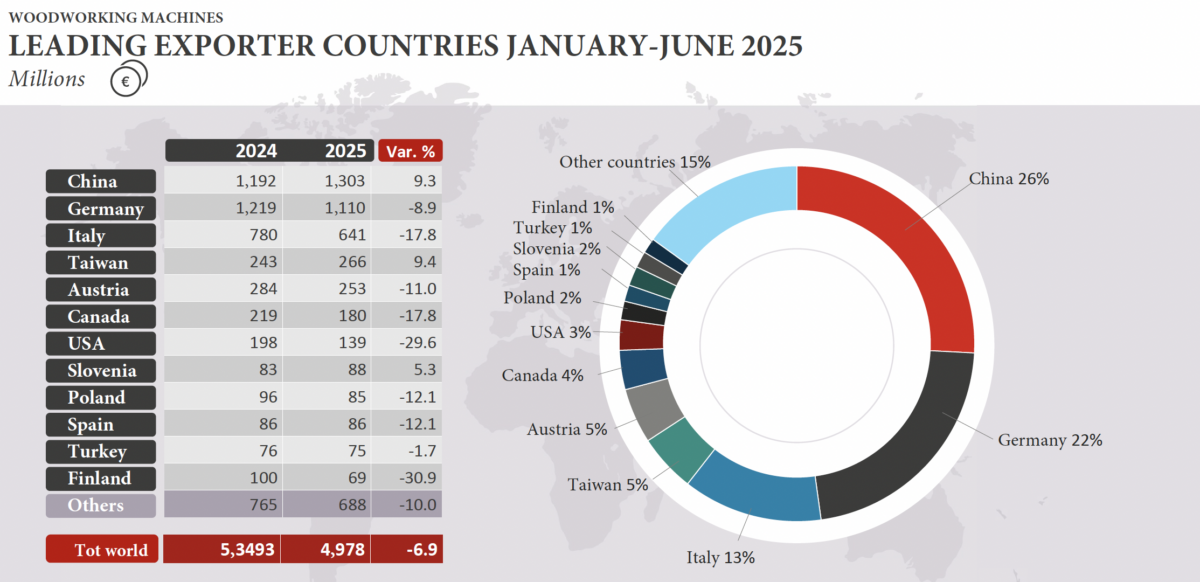

Let us now look at Table 2, which illustrates developments in the latest season based on the most recent global data available. The first consideration concerns the contraction in total global exports, which decreased by 6.9 percent (from €5.34 billion in the first half of 2024 to €4.97 billion in 2025).

Some of the trends already mentioned are confirmed. In the first half of 2025, China reaffirmed its determination, increasing exports from €1,192 million to €1,303 million: up 9.3 percent. These figures bring China to represent, as shown in the chart on the right side of the same table, 26 percent of total global exports.

Germany’s exports in the January–June 2025 period also declined, falling from €1,219 million in the first six months of 2024 to €1,110 million (-8.9 percent). Even more significant is Italy’s contraction, which still accounts for 13 percent of global exports but dropped from €780 million in the first half of 2024 to €641 million in the same period of 2025, a decline of 17.8 percent.

Taiwan holds up well, ranking fourth among exporters in the period considered, with growth of 9.4 percent, while Austria, Canada and the United States lost ground.

INDIVIDUAL COUNTRIES

It is also interesting to look at the tables detailing the performance of the main producing and exporting countries of woodworking technologies across global markets.

Starting with China, which in the first half of 2025 significantly increased exports to Vietnam, Thailand (+42 percent), Brazil, Indonesia, Malaysia and Canada, albeit with very different absolute values.

Sales declined notably in the United States (from €167 million to €129 million, -22.2 percent) and in Germany (-24.3 percent).

Germany shows a certain degree of dynamism despite an economic season heavily affected by uncertainties involving the automotive industry and, consequently, other sectors. Exports in January–June 2025 grew overall: strong sales to China (€133 million compared with €112 million in 2024, +18.9 percent) and to Italy (+43.2 percent); extremely strong growth, in percentage terms, in Thailand and Australia. Less favorable results were recorded in the United States (-30.8 percent) and neighboring Austria (-44.1 percent).

Italy lost ground in China, with exports in the first half of 2025 stopping at €12.9 million, compared with €26.3 million in the same period of 2024 (-50.8 percent). It also declined in France (-33.3 percent), the United Kingdom (-23.3 percent) and Germany (-15.2 percent). The top ten destination countries show a certain “cooling” toward Italian products, with the exception of Canada, where exports rose from €17 million to €18 million.

Finally, let us satisfy our curiosity by taking a look at Turkey, a country often discussed in light of the significant progress made in recent seasons in the production of woodworking machinery and technologies for the furniture industry. However, this evolution has not yet translated into exports, as strong domestic demand absorbs much of the output.

Turkey — which does not appear in the “Top Ten” of exporting countries — shows growth, albeit at clearly modest absolute values, in Saudi Arabia (+87.8 percent), Spain (+66.3 percent), Iraq (+17 percent), Germany (+34.3 percent) and Poland (+32.8 percent). Overall, we are talking about a few tens of millions of euros, but could this signal a new international presence in the coming decades?

METHODOLOGICAL NOTE

The data examined concern all fixed woodworking machines, including spare parts. Portable machines are excluded, as international coding does not provide a breakdown by use on wood. Portable machines intended for processing wood, metal, marble, etc., are grouped under a single generic heading. The above also applies to tools, which therefore do not appear in the following analysis.

CUSTOMS CODES CONSIDERED

8465.10.00

Machines for different operations with manual repositioning of the workpiece for each operation (combined machines) / Machines for different operations without manual repositioning of the workpiece for each operation (multi-operation machines)

8465.20.00

Machining centers capable of carrying out different types of operations with automatic tool change from a magazine or similar device, in accordance with a machining program

8465.91.00

Sawing machines of all kinds

8465.92.00

Planing, milling or shaping machines

8465.93.00

Sanding, grinding or polishing machines

8465.94.00

Bending or assembling machines, including presses

8465.95.00

Drilling and mortising machines

8465.96.00

Splitting, slicing or peeling machines

8465.99.00

Other: wood conditioning machines and auxiliary machinery and equipment related to heading 8465

8479.30.00

Presses for the production of particle board and MDF / others

8466.92.00

Parts and components (spare parts) for fixed machines under heading 8465

Read also...

Nerli: sanding evolves

Assolegno, Daniele Servadio is the new president

Biesse acquires Orchestra Srl

Tecnosalgo presents Edge Tower for automated edge-band management

Rubner celebrates 100 years and invests €42 million in Italy