This year, Centro Studi Industria Leggera (Light Industry Study Center) of Milan turns 45, an opportunity to celebrate the anniversary but above all to look at the present and future of CSIL and the world of furniture.

And to do so, we asked for help from Giovanna Castellina, who joined CSIL in 1999 and is now director of international marketing, as well as being – from 2024 – a “colleague”, because she has also taken over the editorial direction of “World Furniture”, the magazine published by the study center.

“CSIL is the acronym for “Light Industry Study Center”, a definition that we have removed from our current company name to signify the evolution of these years”, Castellina told us. “CSIL was established in May 1980 to deal with research on furniture in Italy, but over the years our investigations have involved more and more countries, until we exceeded the threshold of one hundred markets and today our country represents about 10-15 percent of our turnover.

Not only that: about 25 years ago we activated a second business area, dedicated to the evaluation of EU development projects in collaboration with Italian and foreign institutions. So the acronym has begun to be too small for us, as well as that “Milan” that has always accompanied us but that in the face of our growing commitment across the border…”.

This does not change the fact that the world of wood and furniture continues to consider you a “travel companion”…

“Yes, definitely! The wood-furniture supply chain accounts for about 50 percent of our research, analysis and consulting activities, not to mention that it is the soil in which our roots lie: we have always been, are and will always be proudly part of this supply chain”.

Is economic research more complex than in the past?

“Yes. The internet and, more recently, artificial intelligence represent a challenge that we have to face. A double challenge, I would say, because on the one hand some companies think they can collect the information necessary for their global activities independently, instead of relying on us; on the other hand, our research – which we carry out by going to countries, talking in person with companies and sources that can help us draw up our reports – is uploaded and processed by these systems without any control.

Needless to say, the results, fortunately, are not the same: the direct reports I mentioned, the problems of a correct assessment of the impact on the subject of our studies on conflicts or tariffs that are so much talked about make forecasts and analyses increasingly complex. Our fifty researchers carry out hundreds of interviews every year; we have a database that has over 15 thousand reference contacts in the world of furniture professionals, in all segments of the sector.

Solid foundations from which to look at a season in which geography has a growing weight: I am thinking of the companies that have chosen to relocate to reach the US market and now find themselves having to deal with very high tariffs, which moreover vary or could vary from one day to the next; many Chinese companies have opened production units in Vietnam, others who have chosen Mexico do not know what awaits them. And Europe is wondering how transactions with the United States will evolve, trying to understand what the trend lines of the Chinese economy will be, whether in the near future it will return to growth at the pace of the best years or we will have to wait a little longer… China that is reflecting on the great theme of Asia as its own continental market of reference.

In this context, our researchers find themselves driving blindfolded in the wrong direction!

Not to mention the changes due to the “normal evolutions” of the markets: think of India, a market that according to our “report” of last March has become the fourth country in the world for furniture, with a value of around 22 billion dollars.

In this landscape, increasingly full of unknowns of a different nature, CSIL continues in the wake of its history, made up of rigor, caution, professionalism, knowledge of the markets and their dynamics for an industry – furniture – that we have known for decades”, Giovanna Castellina said.

“We are among the few, for example, who always specify the conditions and economic assumptions that are the starting point of our evaluations, inviting readers to take into due account the possibility of deviations from what we could call an “ideal evolution”, if there were not dozens and dozens of question marks. And what emerges these days is a climate that I could define as “wait and see”, let’s see…”.

Global GDP Development (percent variations)

| Area | 2024 | 2025 |

|---|---|---|

| World | 2.8 | 3.0 |

| Advanced economies | 1.4 | 1.5 |

| Emerging countries | 3.7 | 3.9 |

Source: IMF – International Monetary Fund, “World Economic Outlook”, April 2025

But is the Italian furniture sector defending itself well?

“We are no longer at the top of the ranking of the largest furniture exporters: in recent decades we have been overtaken by Poland and China, but despite all the difficulties, Italy has consolidated its fourth place in the ranking, behind the USA, China and Poland, with imports reaching 19 percent of total furniture sales on the domestic market: we are holding our own, if we want to say so, especially if we compare ourselves with other European countries where imports reach up to 50 percent.

And all this stems from the mass of information that CSIL collects, processes and makes available to a sector in which lighting companies together with furniture industry suppliers, from chemicals to hardware, are among our most active customers, we are talking about dynamic sectors that seek information to guide a strong and continuous innovation process…”.

… perhaps it is also a problem of non-competition, of greater availability of information than in the past…

“We have no competitors who can boast a degree of specialization like ours: in this sense we are artisans who take care of their product in an almost maniacal way. A great effort, I must say, but one that allows us to offer a higher quality than those who analyze the entire world of consumer goods.

Every year, CSIL publishes about forty multi-client reports which are accompanied by “ad hoc” research activities, responding to specific company information needs: we are currently asked for specific advice on the development of new materials or sustainability, as well as support for the evaluation of new markets”.

And what about the next 45 years?

“We are pondering a lot on the issue, because the scenarios – as we said – change quickly. We are small and flexible, and that will undoubtedly be an advantage; we will always remain true to our principles. We asked ourselves the same question during the celebrations for this 45th birthday, and we imagined CSIL in a space suit, with our researchers intent on traveling between galaxies to collect data and information!

So we will be in space, in innovation, keeping intact our independence, our intellectual honesty, our freedom: look, it is not easy to sometimes have to publish “inconvenient” data, which depict a reality that is not what we would like, but this must be a spur to companies to find new spaces and different answers on other fronts.

Knowledge is the basis of progress and this is the terrain on which we have been moving since 1980”.

‘‘World Furniture Outlook 2025/2026’’ report, issued in June 2025

Over the past decade, international trade in furniture has grown more than global furniture production, accounting for about 1 percent of total international trade in manufacturing goods.

By 2019, the trade value of the sector had reached about 151 billion dollars. The outbreak of the pandemic in 2020 interrupted this upward trend. However, 2021 marked a period of strong recovery and growth, followed in 2022 by another year of stagnation. For global furniture trade, 2023 was another quite “tough” year, with a 9 percent reduction. Data for 2024 indicated a modest recovery, with a value of 178 billion dollars.

The outlook has worsened dramatically due to soaring tariffs and trade policy uncertainty that heavily affect global trade and investment decisions. Future prospects are negatively affected by the protectionist agenda of the new U.S. administration.

As a result, world trade in furniture is expected to decline in 2025.

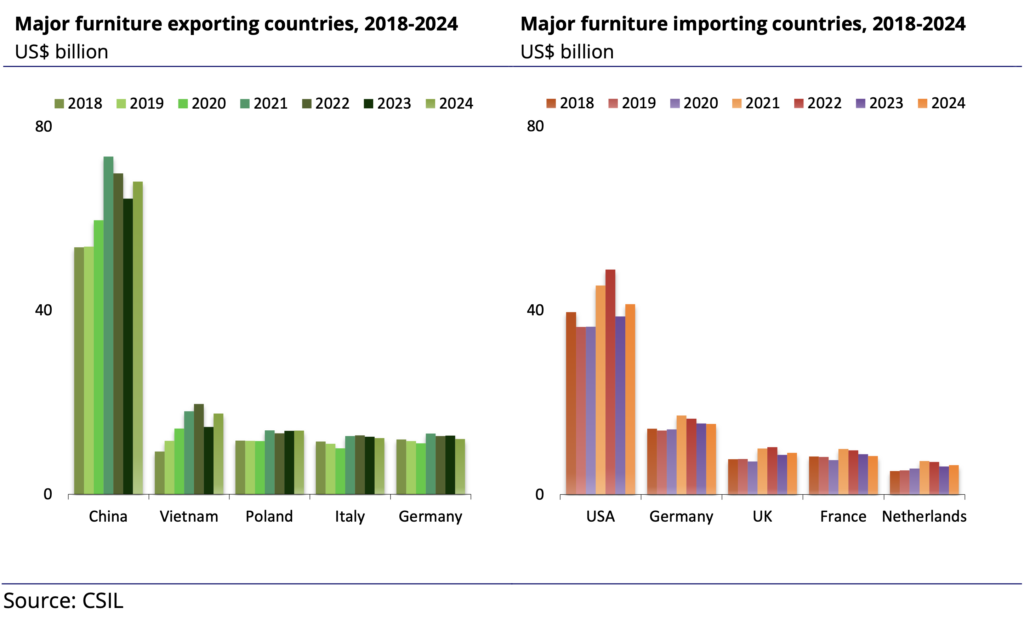

The leading furniture exporter is China, followed at a distance by Vietnam, Poland, Italy and Germany. After a sharp increase in 2021, China’s furniture exports significantly decreased in 2022 and 2023, marking a gradual recovery in 2024. the world’s leading importers of furniture are the United States, Germany, the United Kingdom, France and the Netherlands (a trade hub). U.S. imports account for about a quarter of the world’s furniture imports, at 41 billion dollars.

Of the 100 countries analyzed in the “World Furniture Outlook”, 24 list the United States as their main export destination. Moreover, among these, 10 allocate more than 50 percent of their furniture exports to the U.S. market.

Uncertainty related to international trade policies could push countries to diversify their outlet markets; in particular, trade tensions between the United States and China could generate trade diversion phenomena, raising concerns in markets about possible intensified competition from Chinese exports.

This analysis is based on the values shown in the table “Evolution of world GDP”. According to these figures, world GDP growth is projected to decline by an estimated 3.3 percent in 2024 and 2.8 percent in 2025, then rebound up by 3 percent in 2026. These projections represent downward revisions from previous forecasts. The downgrades in different countries are mainly due to the direct impact of new trade measures, just as their indirect effects are a consequence of increased uncertainty in economic sentiment.

Reduced household purchasing power caused by inflation and high interest rates, tightening financing conditions, and uncertainties in the economic, social, and political environment affected furniture consumption in 2023 and 2024.

In 2024, furniture consumption was almost back to the same level as in 2019. For the world as a whole (100 countries), furniture consumption is expected to remain almost unchanged in real terms in 2025, marking a modest improvement in 2026.

International furniture trade is going through an unprecedented period of uncertainty. Forecasts of international furniture consumption and trade should therefore be used with caution, particularly for countries where the furniture sector is more open to foreign trade. The continuation of such uncertainty negatively affects the economic climate of the industry, influencing the investment decisions and consumption behavior of households.

World Furniture Outlook 2025/2026

Report by CSIL, June 2025, 27th edition