Acimall Outlook

According to tradition, the Acimall Studies Office has laid down for Xylon the ranking of the business results of wood-related industries in Italy, including “Woodworking technology and more”, “Production of wooden furniture”, “Production of wood-based panels and semifinished materials”, “Production of wooden doors and windows”, “Wooden houses and elements for the construction industry” and “Wood and furniture trade”.

The ranking has been drafted based on the balance sheets available so far, related to 2022, when the positive post-pandemic trends strengthened.

WOODWORKING TECHNOLOGY

The analysis is normally focused on woodworking technology, highlighting their trend compared to previous years, while the rankings for the wood-furniture industry provide an all-round view of the entire industry.

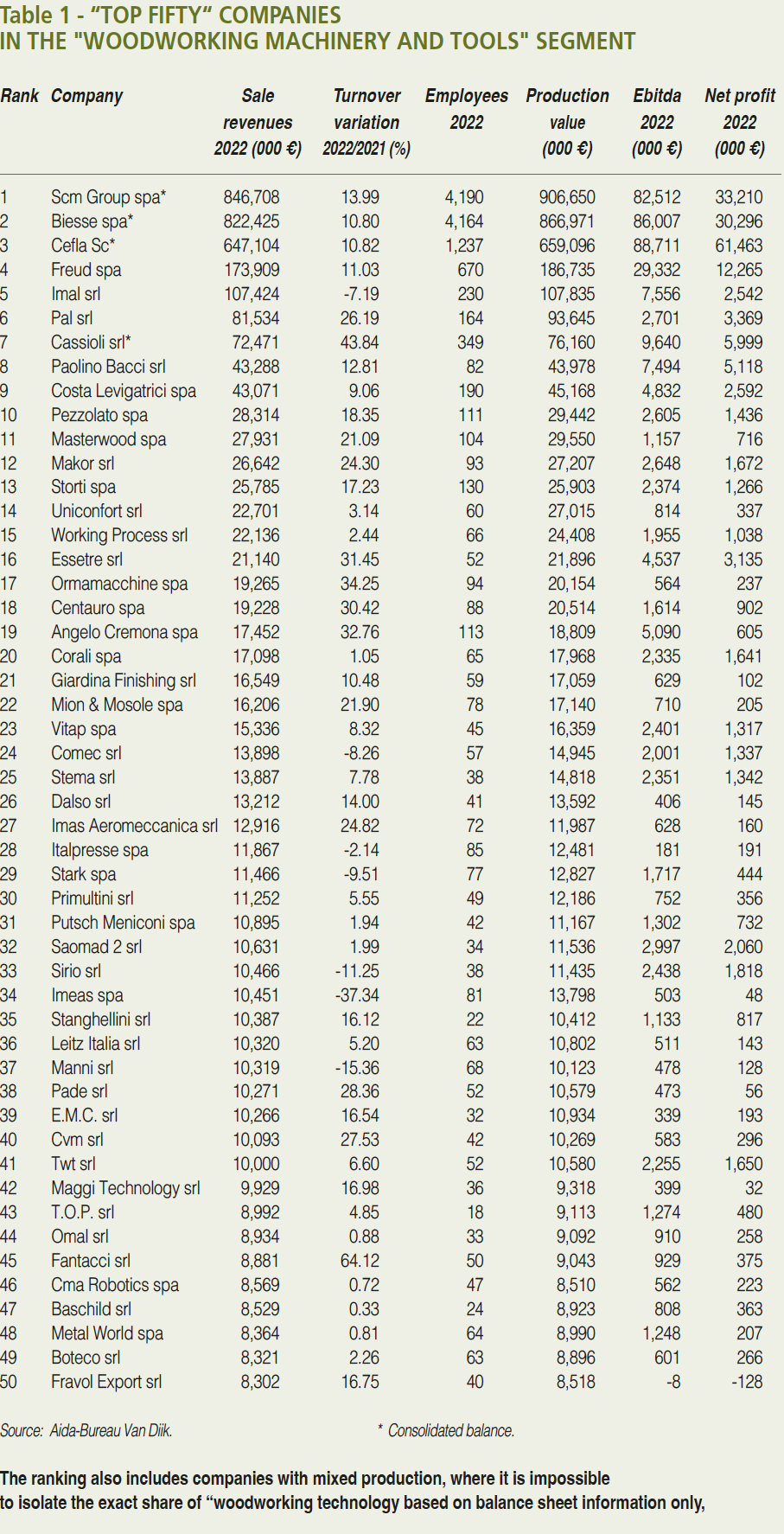

The analysis – takes into account the top-50 Italian companies (Ateco code 2007) by sales revenues in 2 The ranking also includes companies with mixed production, where it is impossible to isolate the exact share of “woodworking technology” based on balance sheet information only.

Scm Group from Rimini, Biesse from Pesaro, and Cefla from Imola take the top-three positions. For the sake of correct information, we point out that the third-ranked company’s core business is not woodworking technology.

The 50 companies listed in the ranking have total revenues of 3,415 million euro, versus 3,064 in 2021, with an average value of 68 million per company (it was 61 in 2021).

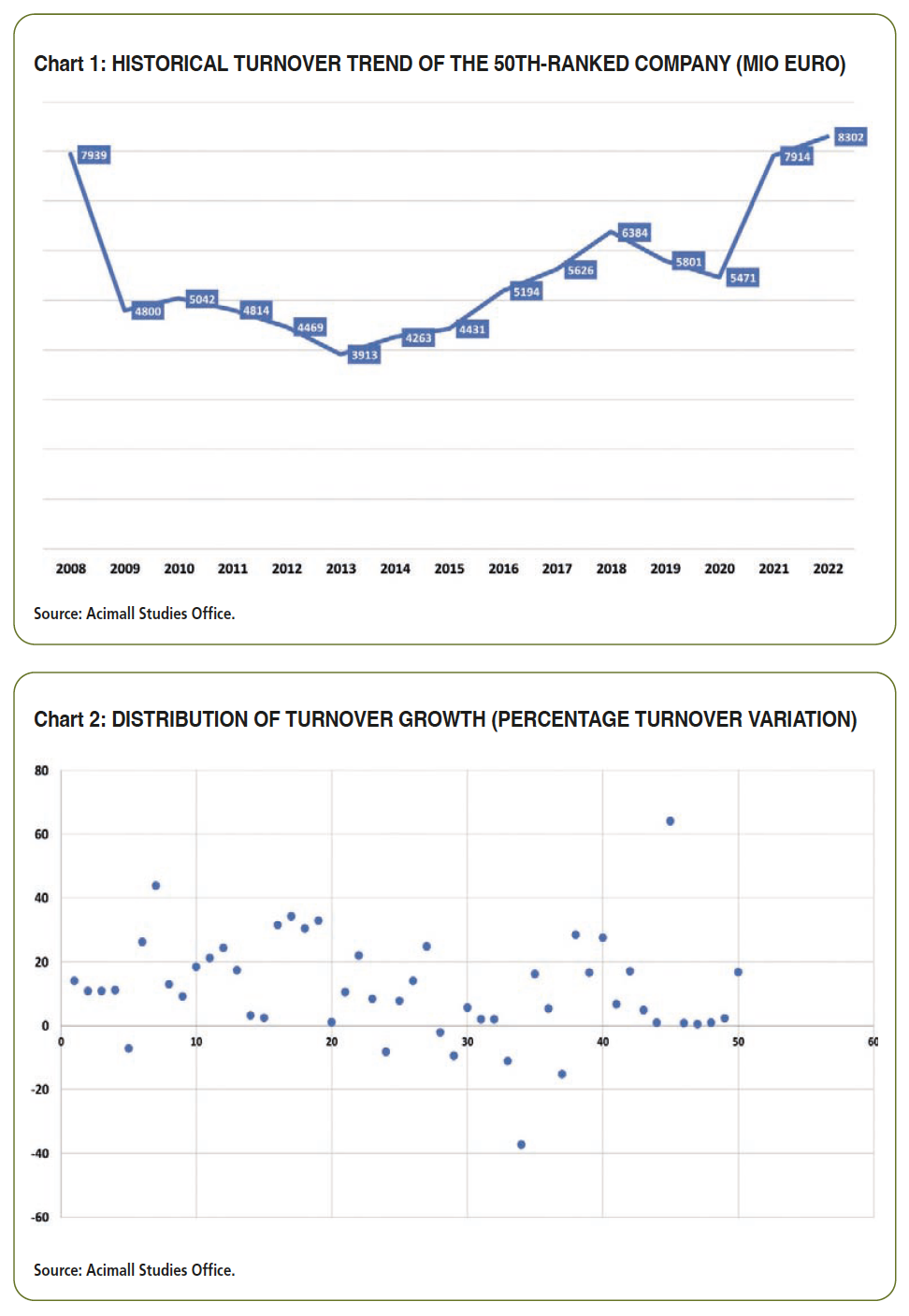

As you can see in chart 1 (on page 14), the revenue level of the 50th company, i.e. the first one above the “entry level” of our ranking, has increased further. One of the key elements emerging from the historical trend of this variable is that, for the first time, the value is higher than in 2008, the year before the financial crisis that struck all the global markets and forced companies to revolutionize their organization models.

Of course, this figure does not consider inflation, which since 2008 has inevitably affected all production costs and not only. This also explains why the current level of small-medium Italian companies is not yet back to pre-crisis levels.

The median, corresponding to the 25th position of the ranking (13,8 million Euro), is higher than the previous year, and the average Ebitda followed the same trend, at 7.5 million euro.

Chart 2 shows a concentration of companies recording increased revenues, even significantly.

2022 AND THE CURRENT ECONOMIC SITUATION

The analysis refers to 2022, so it has a historical value and leaves room for other insights in perspective.

To have a better understanding of the trends, it is necessary to examine the industry development since before the Covid 19 pandemic, and all the consequent events. First of all, it must be observed that the woodworking machinery industry, as well as other segments of mechanical engineering, has always followed a cyclic trend with two-digit growth rates alternating with just as big reductions. What happened in the 2019-2021 three-year period, and also in 2022, was out of the ordinary.

Let’s take a look at the year before the pandemic. In 2019, the industry recorded a 9.9 percent decrease after 10.8 percent growth in 2018, following the alternate trends mentioned above.

In 2020, when the pandemic broke out with its full impact, the industry came to an abrupt halt in the early months, and then recorded strong recovery to close the year with a negative result, but still not so bad as expected in face of the sanitary crisis.

At the end of 2020, the reduction compared to the previous year was 18.4 percent, with a production value of 1.848 billion euro.

The year after, in 2021, the influx of cash into the system and the measures to support the industry and the economy in general caused a positive rebound that we had never seen before. So, 2021 closed with production up by 36.9 percent for a total value of 2.530 billion euro, back to the levels of 2018. At the same time, as we know, the expansion phase was combined with an increase of inflation, also industry-specific.

In 2022, the year under scrutiny in this report, growth continued, though at slower rates, specifically by 4.6 percent. The value of production, gross of inflation, achieved a historical record of 2.646 billion euro, with export amounting to 1.808 and record domestic sales at 338 million euro.

Based on the information above and considering export, Italy’s apparent consumption went far beyond 1.100 billion euro, reaffirming the country’s fourth place in the global ranking.

Looking at the subsequent year and the current one, the industry continued to grow also in 2023 (+3.5 percent over the previous year, achieving new record levels. It is also sensible to expect that the reduction recorded in the latest period will continue in 2024, in a geopolitical situation affected by war in Easter Europe and the Middle East. Some support for the Italian market will also come from the measures of the Industry 5.0 Plan, already approved by the Italian government, waiting for the publication of the related implementing act.

Want to see all the Acimall Outlook rankings? Click here.

Read also...

Imas Aeromeccanica: when extraction becomes a system

Laminate: Europe still central, but 2025 slows down

“Cefla Live”: in Imola from October 6 to 8

From waste to value: the European wood-based panel sector accelerates

Jowat invests in Switzerland: green light for production site expansion