Laminate: Europe still central, but 2025 slows down

Laminate holds in Europe, but declines globally. This is the picture that emerged from the annual conference of the European Producers of Laminate Flooring (Eplf), which brought together producers and stakeholders in Brussels to take stock of a 2025 bluntly described as a “year of adjustment.”

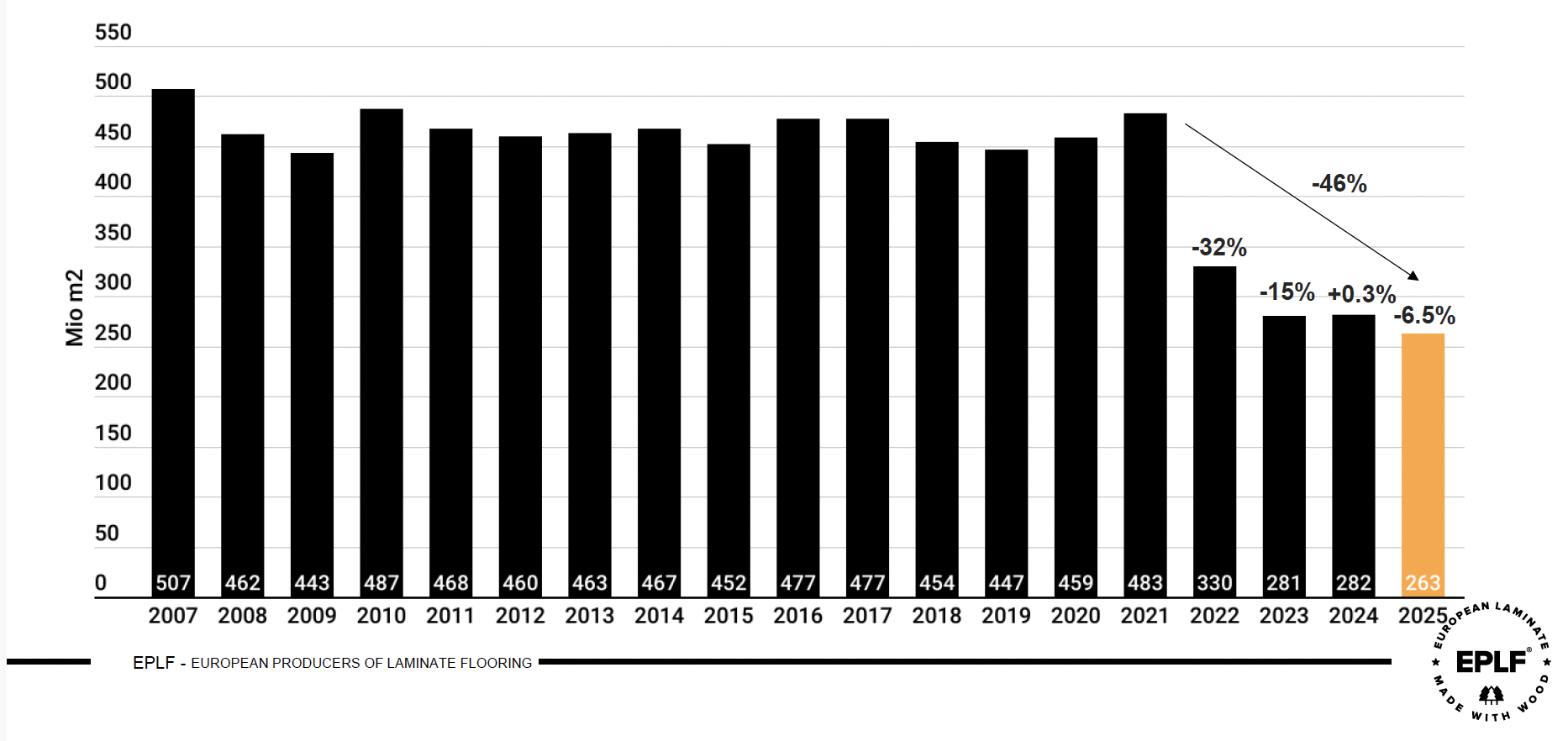

The numbers speak clearly: 263.4 million square meters sold globally by Eplf members, down 6.5 percent from 281.6 million in 2024. A figure that fits into a broader slowdown in the construction sector, amid rising costs, permit delays, and weaker residential activity.

THE NUMBERS

“2025 has been a complex year, marked by economic pressures and a widespread slowdown in the construction sector,” explained Veronique Hoflack, president of Eplf, opening the conference. “But laminate continues to show resilience in its key markets.”

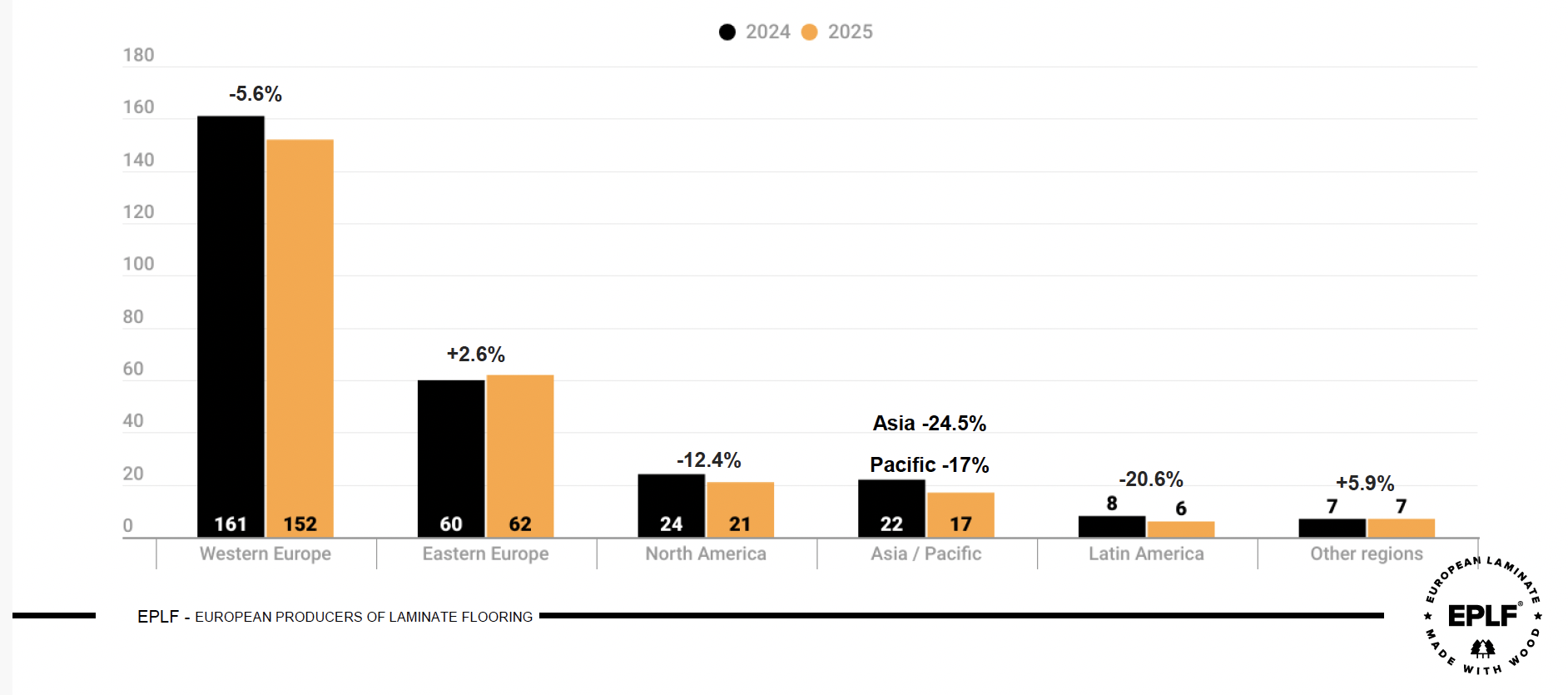

The reference is mainly to Europe, which alone accounts for over 80 percent of total sales. Here, the contraction has been more contained compared to other areas: in Western Europe, which represents 58 percent of the total, volumes reached 151.8 million square meters, down 5.62 percent.

Within the region, France showed substantial stability, reaching 30.4 million square meters (down 0.59 percent), while Germany and the United Kingdom recorded more significant declines, at 8.22 percent and 5.47 percent respectively. The data reflects the different speeds at which national markets are reacting to the economic context and construction sector conditions.

Eastern Europe, on the other hand, confirmed a positive trend, accounting for 23 percent of total Eplf sales with 61.6 million square meters and growth of 2.56 percent compared to the previous year. The region continues to show significant potential, particularly supported by markets such as Poland, which recorded a 3.55 percent increase, and Romania, with growth of 9.3 percent. Alongside these performances, however, more heterogeneous dynamics are observed in other countries in the area, confirming a still evolving landscape.

Outside Europe, the picture appears more complex. North America recorded a contraction of 12.4 percent, while Latin America and Asia showed declines of 20.61 percent and 24.53 percent respectively. In Asia, some of the main markets experienced particularly significant reductions, while Africa showed the sharpest regional decline. Oceania and other smaller markets also recorded reduced volumes, confirming widespread weakening outside the European market.

“The contraction is not uniform,” emphasized Fabian Kölliker, Eplf board member, highlighting how local dynamics and the different states of construction markets significantly affect regional performance.

Despite the difficulties, laminate continues to stand out for its capacity for adaptation and its competitive positioning. The product—Eplf leadership explained during the press conference—maintains strong appeal thanks to its good value for money, application versatility, and increasingly appreciated features such as durability and water resistance. Added to this is growing recognition of its environmental profile: laminate is increasingly perceived as a sustainable solution, based on renewable raw materials and integrated into circular economy models, with a largely European production chain.

A SECTOR UNDER PRESSURE

A “mixed” moment, as the numbers show, but the burden is not only the economic cycle. Data and reports point to a more structural picture, marked by persistent difficulties in the European construction sector. Slow authorization processes and rising costs continue to affect both new builds and renovations, reducing overall demand.

Yet, precisely in this phase, laminate is trying to strengthen its positioning—not only as an accessible solution, but as a product aligned with new European priorities.

“Laminate remains competitive, accessible, and sustainable,” it was reiterated during the presentation, referring to its use of renewable raw materials, predominantly European production, and contribution to climate goals.

**MORE POLICY, LESS PRODUCT**

One of the most evident elements is the growing weight of regulatory issues. Eplf has intensified its commitment on several European dossiers, including the deforestation regulation, circular economy policies, and the development of the digital product passport.

The regulatory framework is set to significantly impact the sector in the coming years. Among the most relevant fronts, the revision of the Blue Angel system (the German environmental label certifying products with high sustainability standards and low environmental impact throughout their lifecycle, ed.) introduces updated criteria for both raw materials and substances used, with stricter requirements on certain chemical components.

At the same time, the new Construction Products Regulation (the European regulation establishing requirements and standards to ensure safety, performance, and transparency of construction products in the EU market, ed.) is set to redefine standards for building materials, with increasing attention not only to technical performance but also to environmental aspects and product durability.

Added to this is the issue of emissions: from 2026, new European limits for formaldehyde will come into force, while the use of other substances such as melamine remains under scrutiny. A set of measures that, overall, will further raise the level of control and quality required in the sector.

These controls go hand in hand with a constant and growing focus on sustainability. The sector is preparing for a phase in which transparency will become a central element, no longer optional.

Among Eplf’s priorities is the updating of environmental product declarations, which must increasingly align with new European tools, starting with the digital passport. At the same time, work is underway to develop shared methodologies for performance assessment, with the aim of ensuring greater comparability and reliability of data.

This marks a shift in laminate’s evolution—from a price-competitive product to a solution increasingly evaluated also in terms of environmental impact across its entire lifecycle.

A BALANCE TO BE RESTORED

For Eplf, the current moment goes beyond a simple cyclical downturn. “We are in a phase of transformation,” observed Philipp Sprockhoff, Eplf board member. “The market is redefining its balance.”

A transformation that also concerns the product itself. Trends for 2026 indicate a clear direction: growing focus on sustainability, development of more water-resistant surfaces, greater durability, and an increasingly central balance between quality and price. From an aesthetic standpoint, larger formats and geometric patterns are gaining ground, in line with the evolution of interior design.

In this scenario, laminate aims to consolidate its role as a solution capable of combining technical performance, economic accessibility, and sustainability. A position that, at least in Europe, continues to prove solid, but will have to face an increasingly competitive global context.

The message that emerges is clear: the future of the sector will not be played out only on the product, but also on the ability to position itself within new European industrial policies.

(f.i.)

eplf.com

Read also...

Nerli: sanding evolves

Assolegno, Daniele Servadio is the new president

Biesse acquires Orchestra Srl

Tecnosalgo presents Edge Tower for automated edge-band management

Rubner celebrates 100 years and invests €42 million in Italy